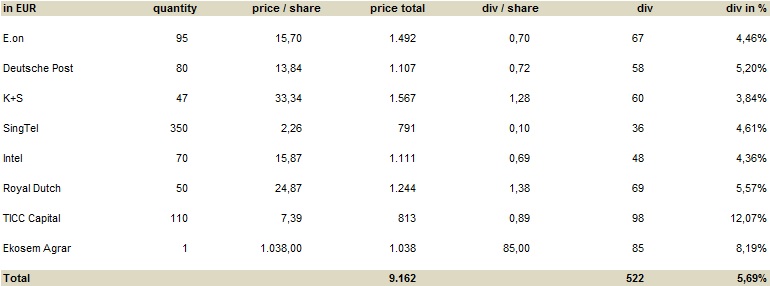

It is time for another market update. Following my August post, I decided not to invest in SingTel and Capitamall and leave my portfolio as it. This did not have to do with the two companies' fundamentals, but rather with general market conditions. Although I have accumulated quite a significant amount of cash reserves, I am of the view that markets have already gone too far. I will therefore stay invested, but will not add any major positions to my portfolio for now.

In the current environment, there are still no alternatives to stocks, but I feel that I was long too late and already missed the biggest part of the rally. In my view, the risk of a market correction is too high and it outweighs the bit of extra return from another investment.

Let’s have a look on the stock indices of my core markets. What has happened since August?

There were German elections in September with the outcome of a great coalition between Christ Democrats (Merkel) and Socialists. Both parties support the EURO policy and will hold a large voting majority (504 of 631 seats) in the Bundestag. Any objections from opposing parties (the Greens and left-wing communist party with together 127 seats) will have no impact on the country’s politics.

There were German elections in September with the outcome of a great coalition between Christ Democrats (Merkel) and Socialists. Both parties support the EURO policy and will hold a large voting majority (504 of 631 seats) in the Bundestag. Any objections from opposing parties (the Greens and left-wing communist party with together 127 seats) will have no impact on the country’s politics. Markets are relieved that the newly founded German anti-EURO party did not make it into the Bundestag. Just like the Liberals, it remained below the 5% threshold with still remarkable 4.8% of total votes. I would have liked the idea of having one party in the Bundestag questioning the EURO policy – even though this would have caused market consternation.

Anyway, it is how it is and as long as there are no exceptional bad news from Southern Europe, the DAX will remain dependend on the Dow Jones which in turn is stimulated by the Fed policy.

This leads us to my next core market, the US. After rumors about a war conflict in Syria, Obama follows a diplomatic approach and now relies on the U.N. to put Assad’s chemical weapons under international control. For the moment it seems as if the risk of a new war conflict is banned.

What about the Fed? Well, as if I already felt it in my last update, the Fed delayed bond tapering as it believes the US economy still needs support. In the end, everything will stay as it is. Nobody expects a slow-down of the USD 85bn monthly stimulus to the US economy still within 2013. For the moment, it seems likely that the Fed stimulus will be maintained for a much longer time. Even if it will be reduced within 2014, I wonder how much longer it will take to completely end it. And more importantly, how will markets react when the Fed announces it will cut or even end the stimulus?

Another factor that has caused market fears was the US government shutdown in October and the potential of a US sovereign default. I did not even had this on my agenda and I guess most people already forgot the last time when a similar situation occurred back in April 2011. Although almost no one expects an US default to occur, there is still no visible solution to the US sovereign debt problem except for ‘kicking the can further down the road’ to the next deadline and hoping for an economic recovery until then. The next funding deadline is Jan. 15, 2014 and the next debt ceiling deadline is Feb. 7, 2014. In the meantime, a congressional committee will work out a longer-term budget deal. It seems as if global markets can rest until then.

Since start of September there was also a remarkable upward correction in the STI and a good opportunity to re-buy cheap has passed. Like markets in Europe and the US, the STI reacted negatively to rumors about tapering of quantitative easing and a pending attack on Syria. Bad news about flattening growth in emerging markets and asia probably also had some impact on the performance. I guess similar to the DAX and DOW JONES, the STI has recovered in the meantime due to the recent positive news trend.

Since start of September there was also a remarkable upward correction in the STI and a good opportunity to re-buy cheap has passed. Like markets in Europe and the US, the STI reacted negatively to rumors about tapering of quantitative easing and a pending attack on Syria. Bad news about flattening growth in emerging markets and asia probably also had some impact on the performance. I guess similar to the DAX and DOW JONES, the STI has recovered in the meantime due to the recent positive news trend.Having said this, it is quite fascinating to see how interdependent all markets are and how important the US monetary policy has become for the world economy. It is this market property which makes me a bit thoughtful about the overall developments. Do prices currently really reflect the intrinsic value of stocks or has everyone just become really desperate about the lack of alternative investment opportunities?

Let's see where the journey of unprecedented loose monetary policy leads us by the end of the year. It seems as if we have new market records in front of us, but the key question is for how much longer...

As usual, the media associated the tapering of QE and the pending attack on Syria as the causes for the correction. - See more at: http://www.bigfatpurse.com/2013/09/singapore-permanent-portfolio-update-aug-2013/#sthash.CZVmwtil.dpuf

{kind=link}